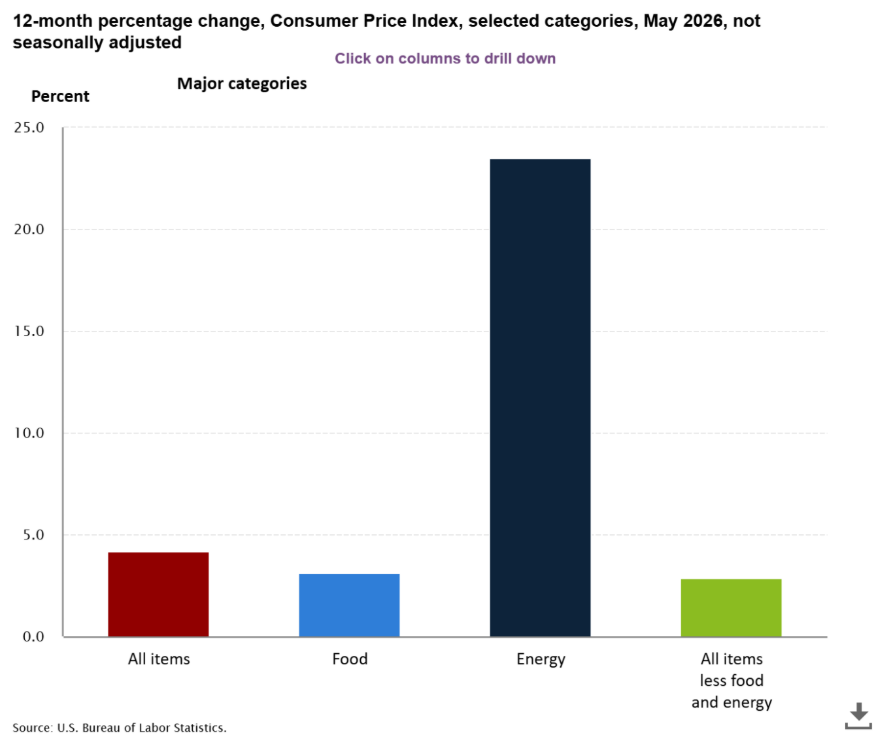

Inflation continues to be the skunk at the garden party. The Consumer Price Index (CPI) for all items was released on Wednesday at 0.5% for May and 4.2% over the last 12 months. This met estimates. If you drill down into the numbers, most of the increase is from energy prices which are up 23.5% over the last 12 months. Core CPI, which excludes food and energy, rose 2.9%.

Add inflation to the strong jobs numbers from last week, and it will be very difficult for the Federal Reserve to cut interest rates anytime soon. Next week, June 16th and 17th, will be the first Fed meeting with Kevin Warsh presiding as the Fed Chair. The assumption has been that he would be in favor of easing monetary policy with lower interest rates. He has argued that the productivity gains that will be achieved with the implementation of AI would allow the economy to produce more without inflation. That may prove true over the long term, but presently, inflation remains a challenge and could keep the Fed from cutting rates—or even force policymakers to consider additional hikes.

The market volatility over the last week has been due, in part, to the shifting assumptions on interest rates. At the beginning of the year, there was an expectation of at least one rate cut in 2026, if not more. With the current economic data, the Fed will most likely keep rates steady at their next meeting but the chances of a rate hike in 2026 are now being priced into the market. Consumer Price Index Inflation 4.2% in May

Changes in the Auto Industry

First, I must admit that I am not a car person, so I don’t usually pay much attention to what the auto makers are doing. But this trend caught my eye because it appears to be a smart strategic move. Several major automakers, including Ford and GM, are expanding into the energy sector. Ford and GM launched new subsidiaries Ford Energy (2026) and GM Energy (2022). Both companies are looking at ways to increase revenue by using EV battery technology for stationary energy storage to help power the increasing needs of data centers.

Some of the benefits of these initiatives are:

- Higher-growth markets - energy storage for utilities, data centers, and renewable energy are growing rapidly.

- Supply-chain control – batteries account for a significant share of EV costs, so controlling production can improve margins and reduce risk.

- New revenue streams:

-

- Grid-scale energy storage.

- Home energy systems.

- Vehicle-to-grid (V2G) services.

- Battery recycling.

- Battery licensing and technology sales.

The automotive industry looks to be evolving into an automotive-and-energy industry. Companies such as GM and Ford are no longer viewing batteries solely as vehicle components but as assets that can support businesses in energy storage, grid management, and battery recycling. This is creating growth opportunities beyond car sales. GM bets on battery storage Ford Energy GM Energy

Financial Planning/Investment Strategy Corner:

Inherited IRA Planning:

Since the SECURE Act became effective in 2020, most non-spouse beneficiaries can no longer stretch IRA distributions over their lifetime. Instead, inherited IRAs generally must be fully distributed within 10 years. That can force beneficiaries to take large taxable withdrawals sometimes during their highest earning years. Since the SECURE Act was passed, we have been helping clients navigate these changes and identify planning opportunities within the rules. One such strategy is the use of disclaimers. Disclaiming

One idea we are suggesting to some clients, depending on circumstances, is to disclaim a portion of the inheritance. A qualified disclaimer can change who is treated as the beneficiary. The disclaiming beneficiary is treated as though they predeceased the IRA owner. The IRA then passes to the next beneficiary. That is the simple version. What we have been suggesting is disclaiming a portion of the IRA so that the primary beneficiary receives what they need and the contingent beneficiary receives the balance of the IRA. This can create two separate 10-year distribution windows for the contingent beneficiary. Here’s an example:

Without Disclaiming:

- Dad has a $500k IRA. Mom is the primary beneficiary and daughter is the contingent. Mom also has a $500k IRA with dad as primary beneficiary and daughter as contingent.

- Dad passes away and mom receives his $500k IRA and since she is the spouse the IRA can be added to hers and she can take distributions over her lifetime. She now has a $1MM IRA.

- Mom then passes away. Daughter inherits a $1MM IRA and is forced to distribute the IRA over a maximum of 10 years. That is $1MM of taxable income over 10 years.

- The 10 years are often during the highest earning years, and the IRA distributions added to daughter’s income can push her into higher tax brackets, sending more of her parents’ IRAs to the government.

With Disclaiming:

- Dad has a $500k IRA. Mom is the primary beneficiary and daughter is the contingent. Mom also has a $500k IRA with dad as primary beneficiary and daughter as contingent.

- Dad passes away. Mom decides that she has enough assets and income for her lifetime without dad’s IRA. She disclaims dad’s IRA and it passes to daughter. Daughter’s 10-year term for dad’s IRA begins at dad’s death.

- Mom lives 6 more years and then passes away. Daughter inherits mom’s IRA and starts a new 10-year window.

- Daughter ultimately inherits the same $1MM IRA, but instead of one 10-year distribution window, she benefits from two separate distribution periods spanning 16 years.

This is a simple example and does not include any change in the account size due to market gains/losses or withdrawals.

Other Things to Consider:

- Disclaiming can be better than naming someone as co-primary beneficiary by keeping the decision to the last minute in case your circumstances change.

- You can disclaim up to 9 months after the death of the IRA owner as long as you don’t take withdrawals from the IRA.

- Disclaiming must be done in writing and is irrevocable.

- Partial disclaimers are permitted. You can disclaim just a portion of the IRA.

Quick Hits:

- Father’s Day is next weekend (June 21), so we still have time! The 37 Best Father’s Day Gifts of 2026 Fun Things to Do on Father's Day 2026

- Tina Fey (with a lot of help) adapted a show from the original Alan Alda film The Four Seasons. Season two just dropped on Netflix. I remember the original (yes, I am that old) and enjoyed the new version. Tina Fey's The Four Seasons Season 2

- The World Cup officially kicked off on Thursday (pun intended 😊). Here is the schedule: 2026 FIFA World Cup Schedule - ESPN

- Maine food at its best: Tootie’s Tempeh, Bixby Chocolate among Maine winners in national food awards

- Am I the only one who doesn’t understand the hype? It’s just chicken! Chick-fil-A to open third Maine location

Artemis III:

Continuing my Artemis coverage, this makes three newsletters in a row! NASA announced the next Artemis mission for 2027. There are four crew members – three Americans and one Italian. They will be testing systems needed for future lunar landings, which are expected to begin with Artemis IV in 2028. This mission will demonstrate and test rendezvous and docking capabilities of one or both of the landing systems currently being developed by Blue Origin and SpaceX. NASA Marches Toward Artemis III Mission in 2027, Names Crew Members - NASA

A Few Summer Quotes:

- “I wonder what it would be like to live in a world where it was always June.” —Lucy Maud Montgomery

- “Summer—the time when parents realize how underpaid teachers actually are.” —Unknown

- “It’s a smile, it’s a kiss, it’s a sip of wine … It’s summertime!” — Kenny Chesney

Thank You for Reading

Thank you for being part of the RSWA community and for reading Financial Advisor Insights! We welcome your feedback — and please share this with a friend or colleague who might enjoy it.

Be well, take care, and stay safe!